Most UCC filing mistakes do not announce themselves. There is no rejection email, no warning from the Secretary of State, and no immediate consequence. The filing goes through, gets stamped, and sits quietly in the public record, looking perfectly fine, right up until the moment your borrower defaults or files for bankruptcy. Then, suddenly, what looked like a secure position becomes contested. Or worse, an unsecured one.

That is the real danger with UCC errors. The cost is invisible until it is catastrophic.

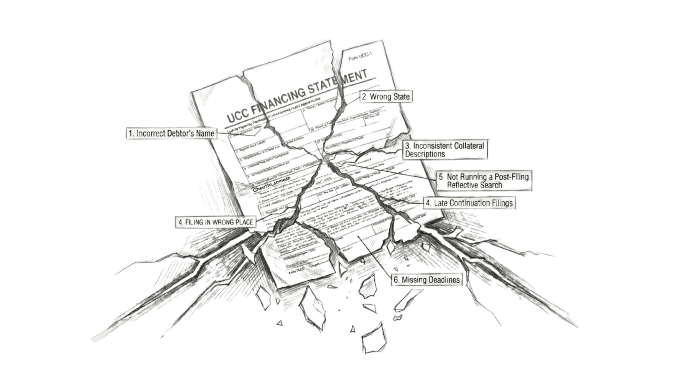

If you are a lender, lessor, credit manager, or anyone filing UCC-1 financing statements to protect a security interest, this article is for you. These are the five mistakes we see most often, what makes each one so damaging, and how to prevent them before they put your collateral at risk.

What Is a UCC Filing and Why Accuracy Matters So Much

A UCC-1 financing statement is your public notice to the world that you hold a security interest in a debtor's personal property. Under Article 9 of the Uniform Commercial Code, filing that statement with the correct Secretary of State perfects your security interest and establishes your priority against competing creditors.

The catch: perfection is not forgiving. A minor error, a missing middle initial, a wrong state, a vague collateral description, can render your filing "seriously misleading" under Section 9-506 of the UCC. And if a court finds your financing statement seriously misleading, your security interest may be treated as if it were never perfected at all.

In a bankruptcy proceeding, this means you lose your secured status and become an unsecured creditor. The takeaway: a small error can change your entire bankruptcy recovery.

Mistake #1: Getting the Debtor's Name Wrong

This is the most frequent and most serious UCC filing error. Even experienced credit teams encounter it, not due to carelessness, but because the requirements are more stringent than many expect.

Under Article 9-503, for registered organizations, the UCC-1 name must exactly match the public record in the debtor's state of formation, not what is on the website or contract.

That means if the state record says "Acme Solutions Incorporated," you cannot use "Acme Solutions Inc." The difference between "Incorporated" and "Inc." has been litigated in real cases. Secured parties have lost priority as a result.

For individuals, state rules vary. Some require the name as on a driver’s license; others use different standards. Nicknames, transposed names, or missing required middle names can make your filing fatally vulnerable.

The solution is straightforward: always obtain the debtor's exact legal name from the Secretary of State's records before filing. Never rely solely on borrower documents. Key takeaway: verify for yourself to avoid fatal mistakes.

By leveraging CoverPin's UCC search and filing service, you can mitigate this risk. Next, we address another common source of error: choosing the wrong filing jurisdiction.

Mistake #2: Filing in the Wrong State

Under Article 9 of the UCC, UCC-1 filings for most debtor types must be made in the state where the debtor is located, not where the lender is located, and not necessarily where the collateral is located.

For registered organizations, file in the state of formation. Lenders often err when a company operates in another state or has recently changed entity type, altering the correct jurisdiction.

Fixture filings are another common source of confusion. Certain collateral, such as equipment attached to real property, may require a separate fixture filing in the county where the property is located, in addition to, or instead of, a state-level UCC-1.

Filing in the wrong jurisdiction can leave your statement unrecognized and your priority lost to properly filed creditors, even if they file later.

Before you file, always confirm the debtor type, the state of formation or organization, and whether collateral requires special fixture filings. Key takeaway: jurisdiction is determined by the debtor and the collateral, not by the lender or location.

Mistake #3: Vague or Inconsistent Collateral Descriptions

A collateral description that’s too broad, vague, or inconsistent with the security agreement creates real risk.

Courts have challenged vague collateral descriptions, such as "equipment" or "all assets," that lack specificity. If your description does not match the security agreement, the filing may not accurately reflect the transaction.

Be specific but not unnecessarily restrictive in collateral descriptions. For equipment, include make, model, serial numbers, and VINs. For inventory and receivables, use the same classification language as in the security agreement. If covering after-acquired property, explicitly state “now owned or hereafter acquired.” Apply these standards to strengthen your filing.

A description that is too narrow may leave assets unprotected, and one that is too vague can be challenged. Both create risk if a borrower defaults.

Mistake #4: Missing or Late Continuation Filings

UCC-1 financing statements do not last forever. Under Section 9-515 of the UCC, a standard financing statement is effective for five years from the date of filing. To keep the security interest perfected beyond that window, the secured party must file a UCC-3 continuation statement.

Here is where the process gets punishing: the continuation statement can be filed only during the six-month window immediately preceding the lapse date. File too early, and it is rejected. Miss the window entirely, and the original financing statement lapses, the security interest becomes unperfected, and you lose your original priority date.

For organizations managing many UCC filings, manual tracking of deadlines increases the risk of missed continuations and unexpected exposure during critical events.

A systematic approach to deadline management fortifies your security interests. Now, let's consider a step that is often overlooked after filing: the reflective search.

Mistake #5: Not Running a Post-Filing Reflective Search

You filed your UCC-1. It was accepted. Done, right? Not quite.

Filing offices can and do make indexing errors. A filing that was submitted correctly may be indexed incorrectly by the Secretary of State, which means a search under the correct debtor name may not return your financing statement. If another creditor does a UCC search and your filing does not appear in the results, they have no public notice of your prior security interest, and your priority position may be jeopardized.

The solution is to conduct a certified reflective UCC search after filing, to confirm that the financing statement is indexed correctly under the debtor's name in the public record. Key takeaway: always verify your filing was indexed to ensure your public notice.

If the reflective search surfaces an indexing error made by the filing office, Article 9-517 provides some protection for filers, but this is an area where disputes still arise and where the cost of being caught in a contested situation is high.

With filing verification complete, multi-state operations introduce unique UCC compliance complications. Let's explore these broader challenges.

A Note on Multi-State Operations

If your borrowers operate in multiple states or your lending business spans several jurisdictions, UCC compliance becomes significantly more complex. States differ in forms, fees, collateral requirements, and search indexing. Key takeaway: multi-state lenders need a centralized compliance system to reduce risks and errors.

UCC Filing Mistake Prevention Checklist

Before every UCC-1 filing, verify the following:

Debtor name matches the exact public organic record in the state of formation

Filing is submitted to the correct state based on debtor type and Article 9 rules

Collateral description matches the security agreement and is specific enough to be enforceable

After-acquired property language is included if the security agreement contemplates it

Continuation deadline is recorded and added to a monitored tracking system

A reflective search is ordered after the filing is accepted to verify correct indexing

Protect Your Security Interest Before Problems Arise

UCC compliance is an area where the cost of proper management is low, but the cost of errors is extremely high. Remember, even a minor filing mistake can wipe out a strong security interest in bankruptcy. The takeaway: vigilance in UCC management is essential to safeguard your secured position.

CoverPin's UCC search and filing service is designed to address these risks. With same-day electronic filings when available, certified UCC searches, reflective search capabilities, and centralized deadline tracking across all 50 states, CoverPin offers credit teams and lenders a faster, more reliable alternative to manual UCC management.

Manage UCC filing or certified search through CoverPin to ensure your security interests are properly protected. Book a free consultation to learn more.

Frequently Asked Questions

What makes a UCC filing 'seriously misleading' under Article 9?

Under UCC Section 9-506, a financing statement is seriously misleading if the debtor's name is so inaccurate that a standard search under the correct name would not return the filing. The standard is a search-logic test, not a perfect-name test. But in practice, even small discrepancies in registered organization names have been found seriously misleading by courts, particularly when a search engine using standard search logic cannot surface the filing.

How long does a UCC-1 filing last?

A standard UCC-1 financing statement is effective for five years from the date of filing. To keep it effective beyond that, you must file a UCC-3 continuation statement within the six-month window before the lapse date. If you miss that window, the filing lapses, and the security interest becomes unperfected.

Can a filing be corrected after it is accepted?

Errors can be corrected by filing a UCC-3 amendment. However, the amended filing does not change your original priority date for the corrected information, and in some cases, an error may have already been discovered by a competing creditor or a bankruptcy trustee. Proactively correcting errors is always better than correcting them in response to a dispute.

Does filing a UCC-1 guarantee I am a secured creditor in bankruptcy?

Filing is a necessary step toward perfection, but it is not sufficient on its own. The security interest must also have attached correctly, meaning the debtor must have rights in the collateral, value must have been given, and there must be an authenticated security agreement. Both attachment and perfection are required for full enforceability against third parties in bankruptcy.

What is a reflective UCC search, and why does it matter?

A reflective search is a certified UCC search conducted after your filing to confirm that the Secretary of State has correctly indexed it under the debtor's name. It is the only way to verify that a third party searching the public record would actually find your financing statement. Filing offices can and do make indexing errors, and a reflective search is the quality check that catches them.